The low-cost brands are driving growth in the market

Fitness penetration in European countries is on the rise, with a current total of 46 million members of health clubs across the continent. This growth is being driven by increasing health awareness, diversification of the industry in more mature markets, and recognition of fitness as part of people’s lifestyle in younger fitness markets.

In line with this, the largest European fitness club operators continue to grow, with investment companies strongly supporting their expansion. Equipment manufacturers also continue their positive development of recent years.

These are some of the key findings of The European Health and Fitness Market, published at the end of April by EuropeActive – formerly known as the European Health & Fitness Association (EHFA) – in co-operation with Deloitte.

Member headcount At the end of 2013, the 20 leading fitness companies in Europe accounted for a combined total of 7.8 million members – 17 per cent of the estimated total European health club membership.

Market growth and development is strongly driven by the booming low-cost operators – such as Basic-Fit, Fit for Free and Pure Gym – which are expanding their concept of affordable fitness both nationally and in other countries. The most successful player in the discount segment continues to be Germany-based operator McFit, which leads the overall membership ranking: 1.2 million people exercise in its close-on 200 clubs, paying just E19.90 a month for membership. Having opened its first clubs in Italy and Poland in early 2014, the company is expected to resume its growth, which had slowed due to its preparations for international expansion.

In second place in terms of members is Leisure Group Europe, with its two brands: HealthCity and Basic-Fit. Thanks particularly to the rapid expansion of Basic-Fit, the company reached 780,000 members by the end of 2013.

Virgin Active, part of Richard Branson’s Virgin Group, ranks third with 598,000 members. Health & Fitness Nordic – the result of a merger combining the club brands SATS, Elixia, Fresh Fitness and Metropolis – comes in fourth, while Fitness First rounds out the top five by members.

If the announced merger between Pure Gym and The Gym Group in the UK is approved by the competition authorities, the combined company will be a top five candidate in the next year.

In the meantime, 2013’s largest change in rank by membership numbers was for British budget operator Pure Gym, which climbed up nine positions to rank ninth overall, with 300,000 members. German operator clever fit was able to improve by seven positions – the second largest shift – finishing 14th with its 252,000 members.

With 242,000 female members, Curves is the largest special interest operator and ranks 15th in the total membership ranking.

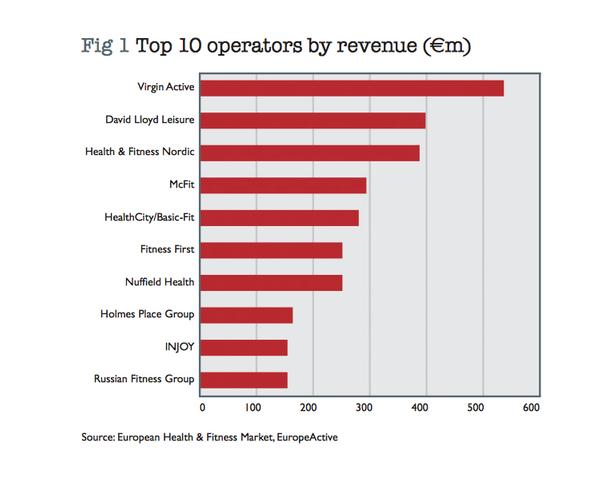

Revenue generators When it comes to revenues, other companies lead the way. Virgin Active is Europe’s market leader (see Figure 1). It operates clubs in the UK, Italy, Spain and Portugal and generates revenues of €532m. In second place is David Lloyd Leisure (€398m), with Leisure Group Europe close behind (€388m). McFit comes in fourth.

“In 2013, the 10 leading fitness companies in Europe brought in total revenues of €2.8bn, and individual operators needed revenues of at least €150m to be in the top 10,” says Niels Gronau, author of the new report and fitness industry expert for Deloitte.

In fact, in terms of total revenue, the European fitness market (€25.3bn) has overtaken the ‘birthplace of fitness’ – the United States – where annual revenues reached €17bn. With the younger European markets also looking set for strong growth, it seems probable that Europe will increase its lead in the coming years. Not surprising, then, that US operators such as Anytime Fitness, Hard Candy Fitness and Equinox have spotted this opportunity and are expanding their concepts into Europe.

“Given the current developments, it’s very likely that the aggregated revenues will grow to over €3bn in 2014,” continues Gronau. “Moreover, particularly driven by the commitments of investment companies, discount operators will extend their presence in the top 10 in the near future.”

One of the latest examples of the ongoing interest of private equity companies in the fitness industry in general, and the low-cost segment in particular, is the acquisition of a 55 per cent share in Basic-Fit by 3i Group. Another example from the budget segment is Nord Holding’s investment in Jumpers Fitness in Germany. Altogether, around 30 deals involving fitness operators have taken place since 2011.

Supplier perspective At the same time, equipment manufacturers were able to benefit from the positive developments among the operators. Indeed, after a substantial drop between 2007 and 2009 due to the economic crisis, aggregated revenues have since recovered and in fact surpassed pre-crisis levels.

Globally and in terms of revenues, the largest operator of commercial fitness equipment is US-based Life Fitness, with revenues of €520m in 2013, followed by the Italian manufacturer Technogym with more than €420m. Altogether, the seven largest international manufacturers have a market share of 50 per cent.

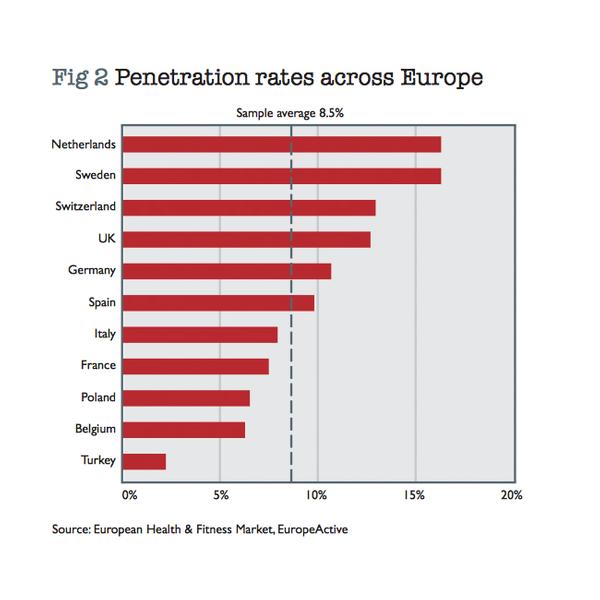

Future potential Turning to individual market performance, Turkey and Poland have the fastest growing fitness industries, with growth rates of more than 20 per cent. While both countries are still relatively new to the fitness landscape, each seems to provide further growth potential, with a fitness penetration rate of only 6.4 per cent in Poland and 2.2 per cent in Turkey. In comparison, the proportion of the population holding club membership in Sweden and the Netherlands amounts to 16.1 per cent and 16.2 per cent respectively (see Figure 2).

“By the end of 2013, 46 million members exercised in one of the 46,500 clubs in Europe. We’re very confident this number will increase significantly in the future,” concludes Herman Rutgers, board member at EuropeActive. “At EuropeActive, our goal is to achieve a total of 80 million members by 2025.”

Fig 1 Top 10 operators by revenue (@m)

Fig 1

Fig 2 Penetration rates across Europe

Fig 2

Read it for yourself....

A copy of the report can be purchased via the EuropeActive website: www.ehfa.eu.com/node/355 Or from sports and leisure consultancy edelhelfer (www.edelhelfer.eu) at http://lei.sr?a=F0B5Q The report costs €95 for EuropeActive members, or €195 for non-members, plus delivery cost.

Leisure Group Europe, which owns Health City and Basic-Fit, has the second largest number of members at 780,000

US brand Anytime fitness has recognised Europe’s potential

Madonna’s Hard Candy already has several European locations

Germany’s McFit is top of the low-cost market

Health & Fitness Nordic ranks fourth in terms of member numbers after a merger

Health & Fitness Nordic ranks fourth in terms of member numbers after a merger

One of the biggest mistakes the fitness industry still makes is advertising almost

exclusively to people who already look and live like gym members. [more...]

Elevate is set to celebrate its 10th anniversary in style this June, with organisers

confirming the event’s largest-ever drinks reception as registrations continue to run more

than 10% ahead of last year. [more...]

+ More featured suppliers

COMPANY PROFILES

Safe Space Lockers

We provide a full turn-key solution for clients from design and consultation, through to bespoke man [more...]

ukactive

ukactive is the UK’s leading trade body for the physical activity sector, bringing together more tha [more...]

The low-cost brands are driving growth in the market

Fitness penetration in European countries is on the rise, with a current total of 46 million members of health clubs across the continent. This growth is being driven by increasing health awareness, diversification of the industry in more mature markets, and recognition of fitness as part of people’s lifestyle in younger fitness markets.

In line with this, the largest European fitness club operators continue to grow, with investment companies strongly supporting their expansion. Equipment manufacturers also continue their positive development of recent years.

These are some of the key findings of The European Health and Fitness Market, published at the end of April by EuropeActive – formerly known as the European Health & Fitness Association (EHFA) – in co-operation with Deloitte.

Member headcount At the end of 2013, the 20 leading fitness companies in Europe accounted for a combined total of 7.8 million members – 17 per cent of the estimated total European health club membership.

Market growth and development is strongly driven by the booming low-cost operators – such as Basic-Fit, Fit for Free and Pure Gym – which are expanding their concept of affordable fitness both nationally and in other countries. The most successful player in the discount segment continues to be Germany-based operator McFit, which leads the overall membership ranking: 1.2 million people exercise in its close-on 200 clubs, paying just E19.90 a month for membership. Having opened its first clubs in Italy and Poland in early 2014, the company is expected to resume its growth, which had slowed due to its preparations for international expansion.

In second place in terms of members is Leisure Group Europe, with its two brands: HealthCity and Basic-Fit. Thanks particularly to the rapid expansion of Basic-Fit, the company reached 780,000 members by the end of 2013.

Virgin Active, part of Richard Branson’s Virgin Group, ranks third with 598,000 members. Health & Fitness Nordic – the result of a merger combining the club brands SATS, Elixia, Fresh Fitness and Metropolis – comes in fourth, while Fitness First rounds out the top five by members.

If the announced merger between Pure Gym and The Gym Group in the UK is approved by the competition authorities, the combined company will be a top five candidate in the next year.

In the meantime, 2013’s largest change in rank by membership numbers was for British budget operator Pure Gym, which climbed up nine positions to rank ninth overall, with 300,000 members. German operator clever fit was able to improve by seven positions – the second largest shift – finishing 14th with its 252,000 members.

With 242,000 female members, Curves is the largest special interest operator and ranks 15th in the total membership ranking.

Revenue generators When it comes to revenues, other companies lead the way. Virgin Active is Europe’s market leader (see Figure 1). It operates clubs in the UK, Italy, Spain and Portugal and generates revenues of €532m. In second place is David Lloyd Leisure (€398m), with Leisure Group Europe close behind (€388m). McFit comes in fourth.

“In 2013, the 10 leading fitness companies in Europe brought in total revenues of €2.8bn, and individual operators needed revenues of at least €150m to be in the top 10,” says Niels Gronau, author of the new report and fitness industry expert for Deloitte.

In fact, in terms of total revenue, the European fitness market (€25.3bn) has overtaken the ‘birthplace of fitness’ – the United States – where annual revenues reached €17bn. With the younger European markets also looking set for strong growth, it seems probable that Europe will increase its lead in the coming years. Not surprising, then, that US operators such as Anytime Fitness, Hard Candy Fitness and Equinox have spotted this opportunity and are expanding their concepts into Europe.

“Given the current developments, it’s very likely that the aggregated revenues will grow to over €3bn in 2014,” continues Gronau. “Moreover, particularly driven by the commitments of investment companies, discount operators will extend their presence in the top 10 in the near future.”

One of the latest examples of the ongoing interest of private equity companies in the fitness industry in general, and the low-cost segment in particular, is the acquisition of a 55 per cent share in Basic-Fit by 3i Group. Another example from the budget segment is Nord Holding’s investment in Jumpers Fitness in Germany. Altogether, around 30 deals involving fitness operators have taken place since 2011.

Supplier perspective At the same time, equipment manufacturers were able to benefit from the positive developments among the operators. Indeed, after a substantial drop between 2007 and 2009 due to the economic crisis, aggregated revenues have since recovered and in fact surpassed pre-crisis levels.

Globally and in terms of revenues, the largest operator of commercial fitness equipment is US-based Life Fitness, with revenues of €520m in 2013, followed by the Italian manufacturer Technogym with more than €420m. Altogether, the seven largest international manufacturers have a market share of 50 per cent.

Future potential Turning to individual market performance, Turkey and Poland have the fastest growing fitness industries, with growth rates of more than 20 per cent. While both countries are still relatively new to the fitness landscape, each seems to provide further growth potential, with a fitness penetration rate of only 6.4 per cent in Poland and 2.2 per cent in Turkey. In comparison, the proportion of the population holding club membership in Sweden and the Netherlands amounts to 16.1 per cent and 16.2 per cent respectively (see Figure 2).

“By the end of 2013, 46 million members exercised in one of the 46,500 clubs in Europe. We’re very confident this number will increase significantly in the future,” concludes Herman Rutgers, board member at EuropeActive. “At EuropeActive, our goal is to achieve a total of 80 million members by 2025.”

Fig 1 Top 10 operators by revenue (@m)

Fig 1

Fig 2 Penetration rates across Europe

Fig 2

Read it for yourself....

A copy of the report can be purchased via the EuropeActive website: www.ehfa.eu.com/node/355 Or from sports and leisure consultancy edelhelfer (www.edelhelfer.eu) at http://lei.sr?a=F0B5Q The report costs €95 for EuropeActive members, or €195 for non-members, plus delivery cost.

Leisure Group Europe, which owns Health City and Basic-Fit, has the second largest number of members at 780,000

US brand Anytime fitness has recognised Europe’s potential

Madonna’s Hard Candy already has several European locations

Germany’s McFit is top of the low-cost market

Health & Fitness Nordic ranks fourth in terms of member numbers after a merger

Health & Fitness Nordic ranks fourth in terms of member numbers after a merger

Global luxury hospitality brand, Six Senses, has partnered with longevity healthcare provider,

HUM2N, to launch a clinic at Six Senses London, at The Whiteley.

Premium London health club, KX Chelsea, will imminently unveil its most significant

redevelopment since its launch in 2002 to create an integrated wellness model combining

training, recovery and relaxation.

Researchers in the US have identified an antibody which could greatly reduce the loss of lean

muscle mass in people who are taking weight-loss medications.

Crunch Fitness has announced the launch of Crunch Reform Pilates – its own reformer concept

designed to bring this fast growing, but rather expensive, modality into the mainstream.

The 20th State of the Industry Report reveals a resilient, expanding and competitive

sector, the

importance of differentiation and the ongoing challenge of tackling inequalities.

Nuffield Health has told HCM that it takes its responsibilities towards its colleagues seriously

and is committed to meeting all legal obligations after news of a tribunal has made national

headlines.

Technogym has announced the launch of the Run X World Treadmill Championship, the first

world championship for running on connected treadmills over five kilometres.

One of the biggest mistakes the fitness industry still makes is advertising almost

exclusively to people who already look and live like gym members. [more...]

Elevate is set to celebrate its 10th anniversary in style this June, with organisers

confirming the event’s largest-ever drinks reception as registrations continue to run more

than 10% ahead of last year. [more...]

+ More featured suppliers

COMPANY PROFILES

Safe Space Lockers We provide a full turn-key solution for clients from design and consultation, through to bespoke man [more...]